According to a study by IHS iSuppli Corporation, in 2010, fabless semiconductor companies expanded their share in the global micro-electromechanical systems (MEMS) market and last year accounted for nearly a quarter of total MEMS operating revenue.

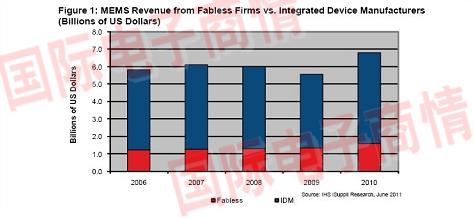

According to a study by IHS iSuppli Corporation, in 2010, fabless semiconductor companies expanded their share in the global micro-electromechanical systems (MEMS) market and last year accounted for nearly a quarter of total MEMS operating revenue. In 2010, fabless semiconductor companies accounted for 23.2% of the total MEMS operating revenue, up from 21.3% four years ago. Although this four-year increase is not large, it shows that the MEMS manufacturing business is no longer monopolized by integrated device manufacturers (IDM) and continues to flow to other vendors. IDM designs and manufactures products internally. In contrast, fabless semiconductor companies, as their name suggests, do not have their own factories, but outsource their manufacturing operations to other specialized manufacturers, foundries.

The figure above shows the MEMS operating revenues of IDM and fabless semiconductor companies from 2006 to 2010.

The most important MEMS device inkjet printhead produced by the fabless semiconductor company accounted for 43% of the waferless manufacturing semiconductor company's MEMS operating revenue in 2010, the largest share, but lower than the 63% in 2006. In this area, Hewlett-Packard outsourced more than half of the print head wafers to STMicroelectronics, and Texas Instruments produced all the printheads entirely from Lexmark International. In addition, the fabless semiconductor company is an unknown printhead manufacturer in mainland China, and cooperates with MEMS foundries such as APM in Taiwan.

The second largest share of waferless manufacturing semiconductor MEMS operating revenue is MEMS pressure sensors, of which nearly one third outsourced manufacturing. For example, in the automotive sector, Sensata, Kavlico, and Melexis partner with various foundries such as SMI, GE, Micralyne, and X-Fab. As for industrial and medical applications, many manufacturers buy dies from foundries and then specialize in packaging.

In third place is MEMS microphones, and fabless semiconductor companies account for 99% of the market. Knowles Electronics is the industry leader, accounting for 85% of the MEMS microphone market, outsourcing all MEMS wafer manufacturing to Sony Kyushu. At the same time, Asiadino outsourced its business to TSMC, and Akustica outsourced MEMS microphones to Seiko Epson.

Optical MEMS is the fourth largest fabless semiconductor MEMS device. It accounts for a large proportion of the operating revenues of professional MEMS foundries such as Micralyne, Dalsa, IMT, and Memscap. These manufacturers have MEMS chip intellectual property rights. Optical MEMS also account for a large proportion of Colibrys’ operating revenue. According to general accounting principles, there are only two IDM vendors in the optical MEMS field - Dicon and Sercalo.

Gyro ranks fifth in fabless manufacturing semiconductor MEMS revenue, and InvenSense has achieved great success in consumer electronics. InvenSense outsourced 2-axis gyroscopes to Dalsa and outsourced 3-axis gyroscopes to Seiko Epson, TSMC and tMt. InvenSense accounted for 97% of the total fabless-free semiconductor gyroscope revenue last year, with the remaining share coming from military and aerospace applications, such as via French foundry Tronics, or from automotive applications through Melexis and foundry partner X-Fab.

Subdivision by Application, Largest Fabless Manufacturing Semiconductor Market 2010 The main application for semiconductorless MEMS is data processing, including inkjet print heads, hard disk timers, and scanning mirrors used in laser printers.

The second largest fabless semiconductor MEMS application is mobile and consumer electronics, and it is also the fastest growing application. Fabless manufacturing semiconductor microphones, gyroscopes and accelerometers are all important components in this field. Automotive is the third largest fabless semiconductor MEMS application, including pressure sensors, microbolometers, thermopiles, and gas sensors.

In terms of size from big to small, other major waferless manufacturing semiconductor MEMS application markets in 2010 included wireline communications, industrial, medical, civilian, and military aviation.

The fabless manufacturing semiconductor MEMS market will continue to grow IHS's forecast that the next five years will continue to grow without wafer semiconductor manufacturing MEMS business, mainly due to a variety of factors conducive to the market.

First, fabless semiconductor startups have introduced more innovative MEMS products that will enter the market. InvenSense is the most successful MEMS startup, but potential hot applications from other vendors are also under development. Among them are SiTime, Discera and Sand9 in the field of timers; Debiotech and CardioMEMS in the healthcare or biotech sector; Microstaq in the industrial and construction control sector.

Second, in the face of pressure from shareholders to maintain high profit margins, IDM and vertically integrated manufacturers may outsource some or all of their MEMS manufacturing operations to fabless semiconductor companies. In fact, several automotive systems companies that traditionally own their own factories, such as Delphi or Continental, have begun or will transition to fabless manufacturing semiconductor manufacturing.

Other factors that will promote the growth of fabless semiconductor MEMS business include the rejuvenation of optical MEMS in telecommunications, optical MEMS as the main source of revenue for various MEMS foundries, and the increasing content of MEMS in mobile phones and tablets. Wireless semiconductor companies have taken note of this trend, but they are not specialized in the MEMS field and will therefore need to align themselves with fabless semiconductor companies to get a slice of it and possibly increase wafer sales.

INT Metal Products Factory , http://www.libometal.com